Valeriya/Getty Images

Just how bad is the national debt crisis? The 12 regional Federal Reserve Banks that compose the largest central bank in the world have a monopoly on printing paper dollars, the world’s reserve currency. Yet despite its ability to print paper and then invest it in bonds, the Federal Reserve is now on pace to lose money on its own scheme to the tune of over $100 billion this year.

Thus, the great bailout institution of last resort has now itself become a further drain on the federal treasury.

Until recently, the Federal Reserve was the ace in the hole for the governing elites who wanted to grow weaponized government on the cheap. The central bank was able to keep interest rates extremely low, which made private borrowers happy but also serviced government debt inexpensively. And by using maturity transformation to borrow short and lend long, the central bank could turn a profit by lending at higher rates of interest than it borrowed. The net profit was always deposited into the rapacious accounts of the Treasury Department to offset a portion of its ballooning debt.

Then came COVID.

COVID ended the Ponzi scheme. In its attempt to permanently control our lives, the Federal Reserve was forced to pay for the lockdowns and ultimately lost control of the money laundering operation. In order to service the debt, the Fed in less than a year purchased $4.7 trillion in additional assets, including $2.5 trillion in mortgage-backed securities. Central bankers invested this money in the form of long-term loans locked in at very low rates.

Then came the inevitable inflation driven by this very COVID spending.

The Federal Reserve was forced to auction so many Treasuries on the market that it had to begin offering higher rates. Many would also argue that Federal Reserve Chairman Jerome Powell raised the federal funds rate too quickly under the false premise that it would stem the tide of the inflation it created.

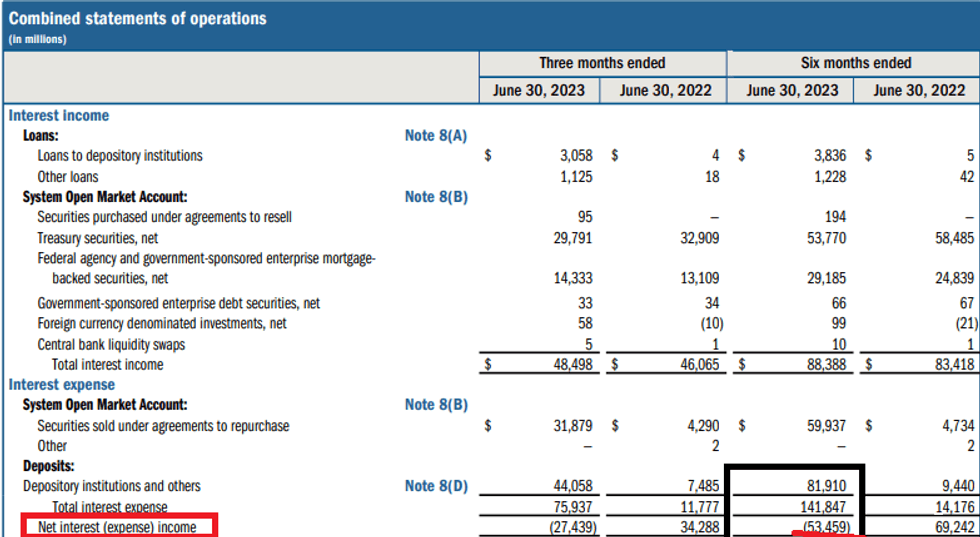

Well, now with interest rates so much higher, the bank is forced to borrow high against all of its prior lending (investments), which was at a much lower rate. We now have the ultimate inversion, which is causing severe deficits. In just the first two quarters of 2023, the Fed has incurred a net loss of $53.5 billion on interest expense, a trend that will only be exacerbated with higher rates, a slowing economy, and a tightening credit market.

The $53 billion loss for the first half of 2023 is on top of the $15.8 billion net loss in the final quarter of 2022.

This is a big deal. For the first time in its more than 100 years of existence, the money god itself can’t print its way out of insolvency.

To print even more money now will take an already tapped-out consumer and small business and crush them further with even higher inflation, tightening of credit, and crushing an already insolvent housing market.

On top of the Fed’s capital deficit is more than $1 trillion in unrealized losses on its $7.6 trillion balance sheet of Treasuries and mortgage-backed securities it purchased in its System Open Market Account. All those assets the bank purchased at 1% interest are now worth much less if the bank were to sell them off at 5.3%. Ironically, this is the same insolvency other banks that come to the Fed for bailouts are facing today.

Yet the Fed simply writes off the loss as it unloads a small portion of its balance sheet (about 9% from its high in 2022) without using mark-to-market accounting, as other banks are required to do under the Dodd-Frank law. Mark-to-market uses the actual market price of the bonds, not the irrelevant face value. The Fed ignores the market price of bonds and assumes they are face value.

If the Fed is incurring this much of a deficit, which will engender more bailouts from the Treasury — rather than the Fed bailing out the debt-ridden Treasury — imagine how the economy will look in the coming years. The majority of FOMC members announced at a Wednesday meeting that they expect another interest rate hike before the end of the year. Then they envision the elevated rates to remain at least for a few years. The capital deficit and unrealized losses on the balance sheet are going to explode exponentially because of the yield inversions, which will further exacerbate the debt tsunami.

Also, even if the Fed itself doesn’t raise the funds rate, the yields on Treasuries must continue to climb just from the sheer volume of issuance the Fed will offload on the market to service biblical levels of interest on the debt, now slated to top $1 trillion every year. There is already a problem attracting enough buyers — with many foreign countries, including China and Japan, dumping U.S. Treasuries. Just wait until these other countries continue with their plan to move away from the U.S. dollar as the reserve currency. Yields will need to increase, further perpetuating and exacerbating the cost of servicing the debt and the Fed’s own fiscal deficit in doing so.

Yields on the two-year Treasury are at the highest level since 2006. However, 17 years ago, the gross debt was $8.5 trillion, not $33 trillion. Also, we were running $200-$400 billion annual deficits, not $2 trillion deficits. Not to mention the fact that we didn’t have nearly this much debt and credit crush in the private sector and among households that are straining banks and individuals to the point of insolvency. Oh, and we are officially not in a recession and have relatively low unemployment. Wait until the fun begins in 2024 and the cost of social programs skyrockets. Even without any new debt, $7.6 trillion of existing debt will mature within the next year at much higher interest rates.

In other words, the Fed, which has been the government’s lifeguard for several generations, is now drowning in the very pool it, along with corrupt politicians in Congress and the Treasury Department, has created. Who will bail out the money printer then?