Huang Evan/Getty Images

Everything you hate about the economy is a direct or indirect effect of our COVID policies. We suffer from “long economic COVID” and will not solve the inflation issue until we understand what got us here.

Inflation is very simply defined as too much money chasing too few goods. Our government decided to spend and then print more money (by a mile) than ever before while shutting down supply chains! Now we are dealing with endless long-term debt and the expense of servicing it, which is inducing even more inflation, forcing interest rates up, and creating the housing crisis we are living with today.

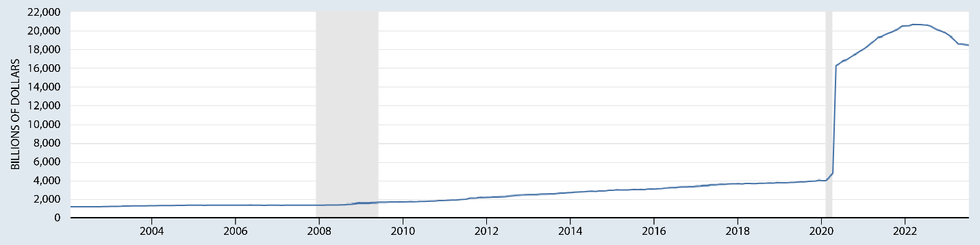

There is no doubt as to the cause of inflation, and it did not begin with Biden, although he has certainly exacerbated it. M1 is the measure the Federal Reserve uses to account for the liquid cash circulating throughout the economy.

As you can see, it rose from about $4 trillion at the beginning of March 2020 to $16.2 trillion by May! It topped out at $20.6 trillion in the spring of 2022, but 84% of that increase in M1 occurred before Biden was sworn into office, when Republicans controlled the White House and the Senate.

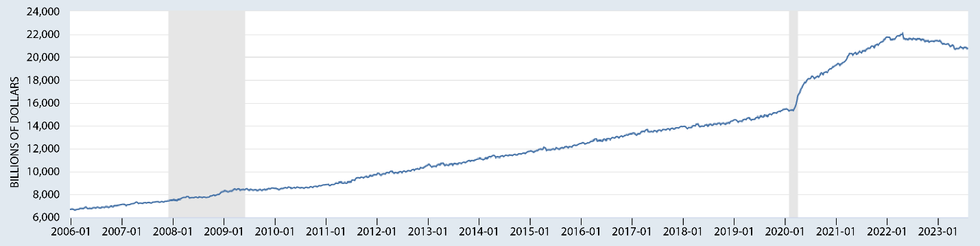

The broader M2 measure of currency in circulation, which includes the slightly less liquid deposits in money markets and CDs, increased 43.7% at its peak, with well over half the increase occurring in 2020. This was simply unprecedented on any level.

Regardless of who would be president in 2021, that inflation cake was baked. Obviously, Biden increased spending even more and locked up our energy supplies, placing more pressure on energy prices. His Ukraine policies made it even worse. However, the core inflation would be with us today regardless of which party is in the White House, because, with few exceptions, both parties equally embraced these terrible policies of loose money.

Now, in order to deal with the crushing inflation and find enough purchasers of all the Treasury bonds to service the biblical levels of debt, interest rates are rising very quickly. This is all a legacy of the housing bubble created by artificially low interest rates, but that same market now cannot deal with even historic levels of interest rates. As such, we are stuck with a housing cliff where most owners are sitting on low mortgage rates but are facing a doubling of their mortgage with a new purchase. This has frozen up inventory, which, for the first time in history, has kept prices extremely high even as mortgage rates go up. In other words, young first-time buyers are priced out of the market.

This is the state of our housing market – all a legacy of the chain reaction of COVID fascism and debt-servicing tactics of the Fed.

In other words, a forgotten legacy of COVID fascism is that it has made finding a new place to live for first-time buyers (or even renters) a luxury. In addition to the manipulation of interest rates, we saw the Federal Reserve service the corrupt debt with $2.7 trillion in purchases of mortgage-backed securities, accounting for 23% of all residential mortgages in the country. This induced the huge housing bubble we are dealing with today. To this day, the central bank has only tapered back the balance sheet of MBSs a mere $200 billion to $2.5 trillion.

Then there are cars. Although the inflation took longer than with housing because the governmental effects were more subtle, the price of cars rose 30% after remaining relatively steady for three decades.

Thus, everything we are dealing with today flows from the CARES Act and its related corrupt descendants passed both under Trump and Biden. It’s not just the immediate shutdown expense, but the permanent long-term expansion of government that is inducing more debt-fueled inflation to this very day. For example, the Families First Coronavirus Response Act, the forerunner to the CARES Act, passed a week earlier, added another 23.2 million people to Medicaid. As such, spending on Medicaid grew by a third in just a few years, topping out at $607 billion this year. Yet despite the end of the pandemic, about three-quarters of that increase is going to be permanent. Now we are going to be paying four times the interest rate on the debt accrued just by the extra $200 billion in spending from one program!

Only 40 House Republicans, mainly in the Freedom Caucus, opposed that bill. Just eight Senate Republicans opposed the bill before it was signed by Trump on March 18. Even if one justifies the initial panic, there was ample time to reverse course for months upon months to eschew lockdown policies and rescind the spending and policy changes to these programs.

So the next time you hear a politician complain about inflation, ask them where they were during COVID.