Photo by Stephen Brashear/Getty Images

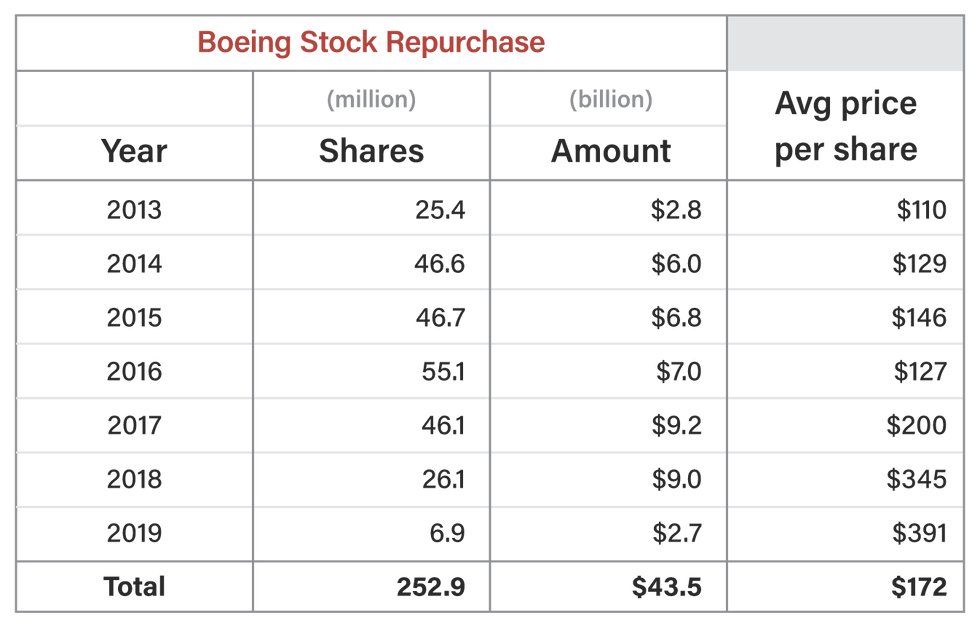

Boeing is a company in crisis and plans to return to the capital markets to raise up to $15 billion in cash to address its liquidity problems. Unfortunately, Boeing squandered over $43 billion on stock buybacks in the previous decade — cash it could desperately use now.

I don’t want to debate the pros and cons of stock repurchases so much as highlight another example of how Boeing’s management, dominated by finance executives fixated on cost reduction and stock valuation, has undermined what was once a leading American engineering and manufacturing company.

In 2018 and 2019 alone, Boeing squandered $11.7 billion of cash to repurchase 33 million shares, which comes out to more than $350 per share. Incredible.

That said, I generally disagree with my pro-capitalism friends on the practice of stock buybacks. I’ve observed for years how harmful this management tactic can be. Companies often conduct stock repurchases when they’re doing well, they are flush with cash, and their stock price is high, using buybacks to further boost the price. But when bad times come and the stock price drops, companies are forced to issue new shares at a much lower price.

The argument for stock repurchases is that a company flush with cash returns excess funds to shareholders by buying back shares. This action increases the value of the remaining stock, as the company’s market capitalization is spread over fewer shares.

The trouble is that the money from buybacks primarily goes to former shareholders — those who sell their stock. In contrast, a dividend would benefit ongoing shareholders. Even better, retaining the cash to invest in the company can lead to better products, new revenue streams, and ultimately higher profits. Other smart alternatives include paying off debt or simply holding the cash for future needs.

But those options don’t provide short-term boosts to stock prices. Not coincidentally, today’s senior executives often receive substantial compensation based on stock performance. In other words, draining a company’s cash reserves through buybacks can help an executive move from earning seven figures to eight figures, but it doesn’t build long-term value or support future growth.

Over the past few years, there has been a litany of awful stories involving Boeing, including planes falling out of the sky, the 737 MAX being grounded, doors blowing out in flight, astronauts being stranded in space, etc. It’s all starting to impact operations and cash flow.

CNBC reported last week that Boeing plans to cut 10% of its workforce, about 17,000 people, amid a machinist strike that has shut down manufacturing for over a month. The launch of Boeing’s critical new 777 variant has now been pushed back until 2026. It’s already several years behind schedule. Boeing has paused flight tests after discovering structural damage in an aircraft.

That’s a polite way of saying the company discovered negligent engineering and poor design. Once upon a time, negligent engineering would have been unthinkable at Boeing. But the business-school types now in charge have long since rid the company management of those who prized high-quality design and production.

According to CNBC:

Boeing expects to report a loss of $9.97 a share in the third quarter, the company said in a surprise release Friday. It expects to report a pretax charge of $3 billion in the commercial airplane unit and $2 billion for its defense business. In preliminary financial results, Boeing said it expects to have an operating cash outflow of $1.3 billion for the third quarter.

Despite all this chaos and neglect, Boeing CEO Dave Calhoun made $32.8 million in total compensation in 2023, up from $22.6 million in 2022.

To be fair, Boeing’s executives have been able to loot the company and redistribute shareholder equity to themselves because Boeing’s board of directors allowed it to happen. They are complicit.

The table below shows a breakout of Boeing’s $43.5 billion in stock repurchases from 2013 to 2019. Of note, the current Boeing stock price is about $150 per share.

Here are a few key observations:

Boeing’s costly and deadly mismanagement, which prioritized cost-cutting and stock price manipulation, would make an excellent case study for business schools. Unfortunately, the very management practices that have so damaged Boeing are the same ones being taught in our elite business schools today.