xavierarnau/Getty Images

Joe Biden last week celebrated his administration’s job data showing 336,000 new jobs created in September. “That’s Bidenomics,” boasted the president — or whoever posted for him — without any self-awareness of the term. He is absolutely correct that there is something unique about the job creation associated with Bidenomics. At its core, what the term means is that debt and inflation are so uncontrollable that people need to seek out second and third jobs just to afford basic needs.

Thus, Bidenomics is the first system in our history that has actually made “job creation” an ominous economic indicator.

Nobody living in the real world feels the economic momentum that would be associated with such a level of job creation. Indeed, ADP’s more accurate employment report, published two days prior to the Bureau of Labor Statistics report and which only includes private-sector jobs, reported only 89,000 new jobs in September. Furthermore, BLS’ other report, the household survey, showed 86,000 new jobs, almost exactly on target with the non-government ADP report.

So what gives? Is the Biden administration cooking the books with the establishment survey showing 336,000 new jobs? I wouldn’t put it past them, but the truth seems to be laid bare in the detailed numbers between part-time and multiple-job holders in the household survey.

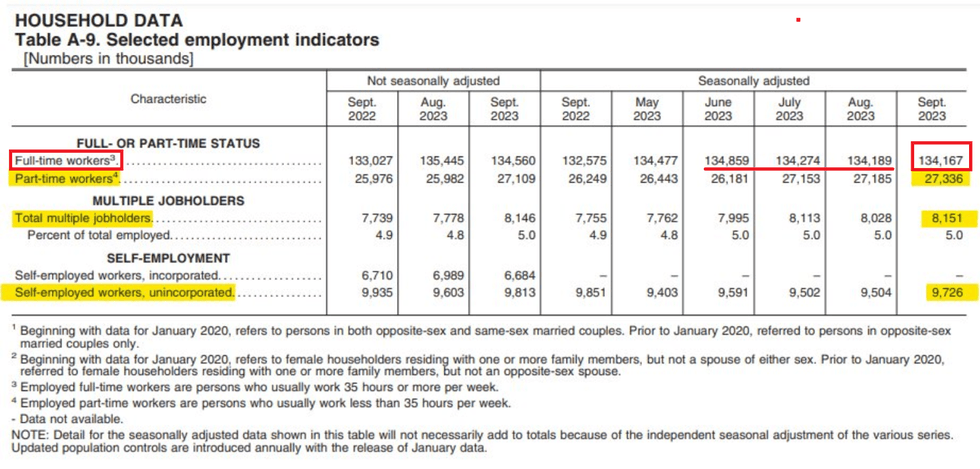

As you can see from the table, not only was there no job growth among full-time jobs, but the numbers actually declined by 22,000 in September and nearly 700,000 since June. That is much more reflective of the economic slowdown we are seeing in the real world, as indicated through the decline in demand for oil.

So where did all the mysterious new jobs come from? An increase in part-time jobs, multiple-job holders, and self-employed workers. The number of part-time workers jumped by 151,000 in September and by a total of more than 1.2 million just since June! Multiple-job holders shot up by 123,000 in September, which makes it very likely that most of the increase in part-time jobs was composed of existing workers taking a second job. That has also been an enduring trend all year. Additionally, the number of self-employed workers grew by 222,000.

In a vacuum, an increase in part-time and multiple-job workers is not a bad thing, but with the fact that the number of full-time workers declined, it demonstrates that this is more out of desperation than profit-seeking. Which means that people are working more not for upward mobility but just to pay the bills. This reality is obvious from the fact that there are a record number of people working two full-time jobs.

This is despite the fact that there have been nearly 700,000 fewer full-time jobs over the past three months. So the pie of full-time jobs is actually shrinking, but those fewer people are consuming multiple jobs and also seeking and even creating more part-time jobs, which would explain the rise in the self-employed.

Hence, the Biden administration is celebrating a symptom of a very destructive trend in which obtaining one solid full-time job is no longer enough for a lot of people to afford living. With mortgage rates approaching 8%, car loan interest rates at their highest in 22 years, and credit card interest rates at a record high, perhaps Biden will continue to “create” a greater demand for more jobs within the same shrinking pie rather than growing the pie itself. It’s why total revenue to the Treasury shrank by 9% in fiscal year 2023, with individual payroll taxes plummeting by 17%, despite all the “job creation.” If the job market and wages were growing the way the Biden administration boasts, we’d see record-high tax revenue.

This trend of working longer to earn less to afford fewer items is likely permanent, because the inflation crisis is getting worse. Remember when we hit the $33 trillion debt milestone on September 15? Well, we are already more than halfway to

the next trillion in less than a month! The debt now stands at more than $33.5 trillion, while the entire economy is only $25.46 trillion. Just one month of debt will now be higher than any full year in American history until the Great Recession in 2008.

Adjusting for the student loan bailout, we essentially racked up a $2 trillion deficit this year. That is the quickest debt accumulation without a world war, pandemic, or recession. And those numbers are still built upon much of the debt serviced with low interest rates. Wait until the new debt matures and has to be refinanced at higher rates.

For example, on Tuesday, the Treasury Department auctioned off $46 billion in Treasuries at nearly 4.7% interest. The cost of financing that debt is $6.54 billion. That is 28 times more expensive than the cost of servicing the same amount of debt during COVID three years ago when rates were close to zero. And now rates are surging to 5.5%.

Our government has lost control over the economy, and inflation is off to the races. But fear not, you will be working multiple jobs to pay bills — and nothing more — until you die. Embrace the power of Bidenomics.