© 2026 Blaze Media LLC. All rights reserved.

Obamacare is ubiquitously regarded as an utter failure. However, when viewed through the lens of its supporters, it is a smashing success. The goal of Obamacare was to ensure that no average-income family (or even upper-middle income family) could live in dignity without government subsidies for health insurance. By that measure, the leviathan has achieved its goal. Will we the people let them get away with it?

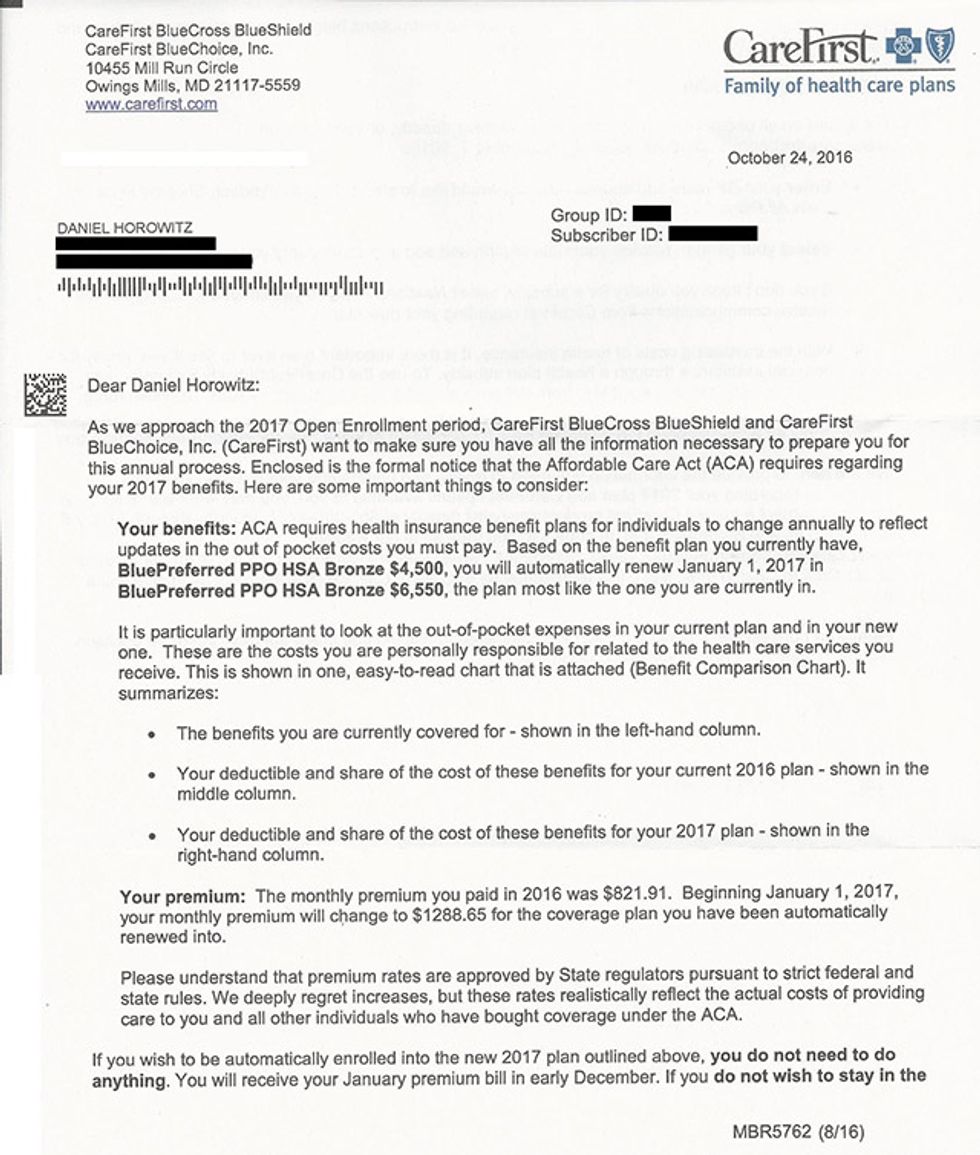

Like millions of other Americans, my wife and I just got the dreaded Obamacare letter in the mail, and it ain’t pretty:

My monthly premium for the HSA Bronze plan under CareFirst Blue Cross Blue Shield of Maryland will be going up from the already astronomical $821.91 a month to $1288.65. Worse, the deductible, which was already high, is going up to $13,100. It is an incredible testament to our broken political system the fact that the Republican Party has barely made this an issue during the past two presidential elections. The Obamacare crisis is a once-in-a-generation opportunity for conservatives to win the fight over government intervention once and for all.

To begin with, the price of health care and health insurance was always distorted and inflated thanks to a myriad of government regulations, the employer-based tax exemption (what I refer to as fourth party coverage), and other cultural trends of over-utilizing and over-insuring health care. Nonetheless, there was enough choice and competition in the market for most Americans to find a tailor-made plan that more or less worked for the family at a price that would not place a crushing burden on the family budget.

My Pre-Obamacare Plan

Prior to enactment of Obamacare regulations, my family of five had a plan with a monthly premium of $425. The “Healthy Blue” plan from CareFirst of Maryland had a $5,000 deductible, but it covered most of the basic necessities for absolutely free, even before meeting the deductible. All sick and well visits to the primary care physician were covered 100% without copay, as were generic prescription drugs. Specialists were covered with just a $40 co-pay before meeting the deductible. For a healthy family with three young kids in which ear infections are the most common ailment, this plan worked out perfectly because sick PCP visits and generic drugs account for most of the expenses.

Even under this relatively high deductible plan, I was able to have surgery to remove two Lipomas from my abdomen for just $40 because it was done in the office of the surgeon. Hospitalization was obviously not covered, but that was a worthwhile calculated risk given the money we saved on the premiums. Plus, the deductible, although relatively high (now we’d die for it!), would be met by the time potential extended health costs would surpass the sum we were saving from the cheaper premiums. Those are the decisions that smart families make every day on an array of goods and services when there are actually market-based forces allowing competing offers from which to choose.

The crushing increase in costs in just a few years

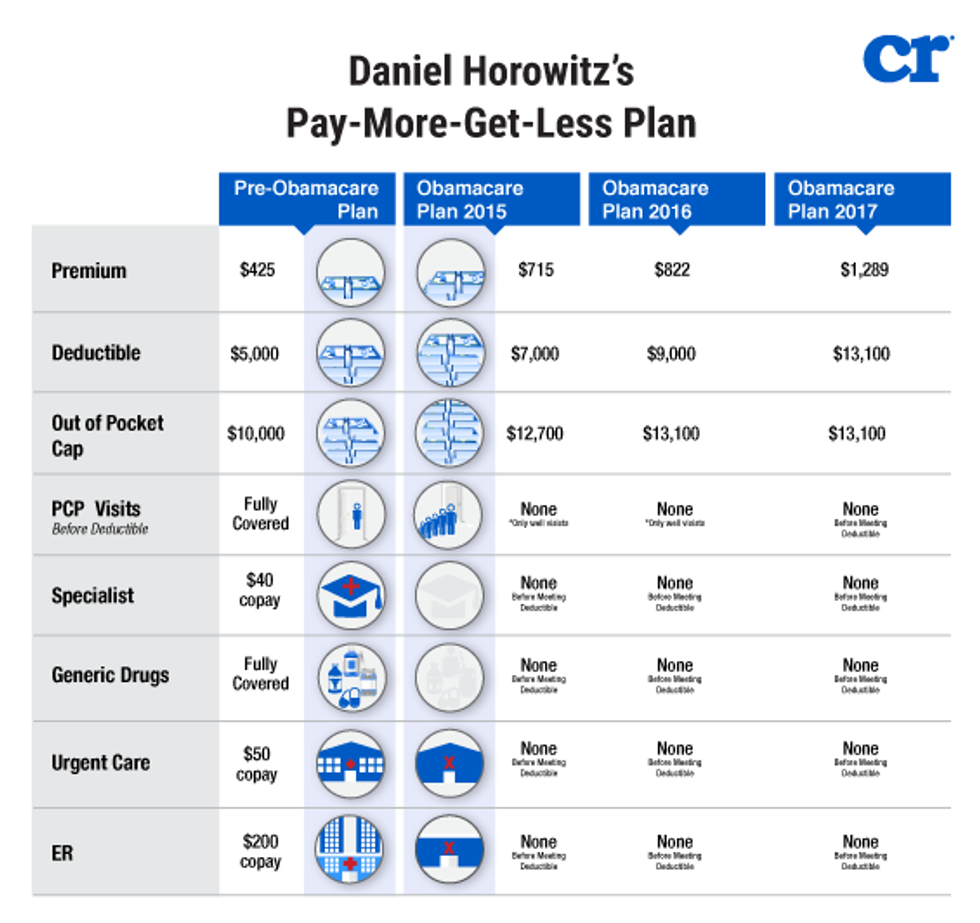

Now, take a look at this graphic for a vivid demonstration of what Obamacare has done to our budget:

Our premium has tripled to a crushing cost of $1,288 per month, over $15,000 a year. Just this year’s increase alone will be $467 a month, $5,600 a year. Remember, my entire premium was less than $5,000 before Obamacare. And what do we get for the crushing cost? We pay money in order to pay money. The deductible has gone from $5,000 to $13,100, and unlike with our previous plan, nothing but the dubious “annual well visits” are covered prior to meeting the deductible. That means one must shell out roughly $28,000 in a given year before one red cent of routine or emergency medical care is even partially covered.

Thanks to the overutilization and no market forces in healthcare, even a perfectly healthy year for a family of five — with no costs beyond typical sick visits and basic antibiotics for standard ailments (no hospitalizations or ER visits) — we must shell out $3,000-$5,000 in out-of-pocket-costs. Add that to the $10,000 increase in premiums from Obamacare and my family must pay a minimum of $13,000 more a year in health expenses thanks to the stupidity of those who voted for Obama and the perfidy of the Republicans who have no plans to fight it.

Once you let that sink in, take note of the fact that this is just the third year of implementation. What does the price tag look like 3-4 years from now?

This issue is potent enough for a true opposition party to win

A party that was actually committed to sound conservative policy would utilize this as a teachable moment, irrespective of who becomes president. My story is undoubtedly the story of so many families. Whereas most prior big government interventions took longer to inflate the cost of the private sector, and the deleterious effects were not apparent enough to the public, everyone recognizes that Obamacare is the culprit for the health crisis and they know who is to blame. This is one case where families unambiguously feel the cost of regulation and government intervention.

$13,000 is real money. That is a lot more than what we spend on food a year for a family of five. The $467 increase in monthly premiums just from last year’s increase is more than my monthly car payment for our Toyota Sienna. I could by a new minivan for that cost. Recently, we replaced our heating and air conditioning with a top-of-the-line system and I’m only paying about $260 a month for a zero-interest loan. Heck, it’s a lot more than what we pay for our son’s playgroup.

This issue alone could sink the entire Democrat Party in the long run. Yet, the Chamber of Commerce has already made it their official policy to “fix Obamacare” instead of ending it. Watch for Hillary (if elected) to call for single-payer and Republicans to use that as the new baseline to define the contours of their opposition. They will oppose single-payer but offer nothing more than what the Chamber and insurance companies are looking for — a bailout and a preservation of the coverage mandates, such as pre-existing conditions and community rating — the very mandates that have made insurance actuarially insolvent. That has already been the official policy of GOP leaders for years, even though they run on repealing the law.

Rarely do conservatives have an opportunity to demonstrate why unconstitutional government interventions are not just costly for the federal budget (most people don’t understand how the debt affects them) but also for the family budget. This is an opportunity for a new movement to rise up and pledge to fight this law until the bitter end. This issue was responsible for two landslides in midterm elections that were not overpowered by personality issues, as was the case in 2012 and this election.

Republicans will still have control of the House and very possibly the Senate after next week’s election. If every elected Republican — not just Ted Cruz, R-Texas (A, 97%) shouting from the wilderness — would use the power of the purse to put an end to this problem, even a Democrat president could not overcome the pain crying out from the family budget of millions of Americans. And in fact, Hillary Clinton, who will likely enter the presidency as the most illegitimate and unpopular persona since John Quincy Adams, is the most beatable opponent on this issue. If only we had a real second party …

Democrats better be careful what they wish for. The people are not with them on a single major issue, Obamacare first and foremost. This issue will only deteriorate for them in the coming months and Hillary is the polar opposite of Obama’s likable “Teflon” personality. The only thing saving them is a fake Republican Party committed to “governing” with them instead of exposing and defeating them. That will not always be the case. It will change one day. The fight will continue, irrespective of what happens next week. Remember, our republic will not rise or fall on your vote for president alone, but whether you acquiesce to this corrupt system or take your own destiny into your hands.

Editor's Note: This piece has been updated to correct several typographical errors.

Want to leave a tip?

We answer to you. Help keep our content free of advertisers and big tech censorship by leaving a tip today.

Want to join the conversation?

Already a subscriber?