Dimitri Kalvan/Getty Images

It looks like the Biden-McCarthy “Fiscal Responsibility Act of 2023” will rival the Inflation Reduction Act (Green New Deal) in its Orwellian meaning and outcome. Just five weeks after the deal was hatched, the Treasury has issued over $1 trillion in new debt!

This is simply astounding. It took from our founding until 1980 to accrue the amount of debt that we have now added in just over five weeks. It is truly hard to overstate the magnitude and impact of this spending. Unlike in recent years, when we were servicing this debt at 1%-2% interest rates, this new debt will be serviced with an over 5% interest rate! Our debt has increased almost 50% in just four years, topping out near $32.5 trillion, but now it will have a compounding effect with higher interest rates to service it. So this notion that inflation will decrease in the long run is absurd. This debt is not just a number on the government balance sheet. It represents why middle-income Americans will not be able to afford the American dream for the foreseeable future. So no, the debt ceiling deal did not “avoid default,” it accelerated it.

There is no way to avoid the flood of inflation for the foreseeable future. The Federal Reserve will continue printing money to service the debt. The elevated cost of living induced by the money pumping will continue to create political pressure (and market forces) for the Fed to keep interest rates elevated under the ill-conceived notion that it will temper inflation, which further harms consumers, as we see with homes and cars. This, in turn, has created a level of personal household debt we’ve never seen before.

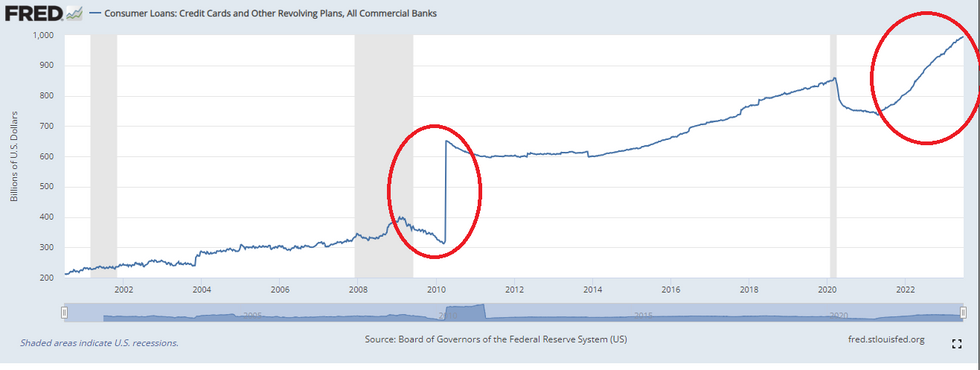

Personal credit card debt is now approaching $1 trillion, up 15% since pre-COVID and more than triple what it was before the Great Recession in 2008.

This is one of many indications that we never recovered from the interventions of Congress and the Federal Reserve since 2008, much less post-COVID. Add to that the fact that average credit card interest rates have now spiked to 22% and the personal debt situation is as bad as the public debt. Now, the conflation of endless federal money pumping creating asset bubbles mixed with relatively high interest rates (in an economy hooked on artificially low interest rates) is inevitably going to shut down the economy.

The unnatural low and then high interest rates all manipulated to service the debt have created a housing crisis. Not only did the Federal Reserve create a housing bubble in order to service the debt with mortgage-backed securities, but it also created a mortgage rate cliff. So new home buyers must pay double the rate, while existing homeowners are sitting on really low interest rates, thereby precluding them from selling their houses. This has created a housing shortage keeping prices artificially high. With mortgage rates topping 7.38%, the average monthly payment on a $400,000 home is the same it was for a $700K home when Biden took office.

Ultimately, the only way prices will come down significantly is if there’s a recession. The good news on that front is that this might be around the corner within the next 12 months. All the constant monetary manipulation policies of the Fed that induce misallocation of resources – all to deal with the money printing scheme – will further weaken the economy.

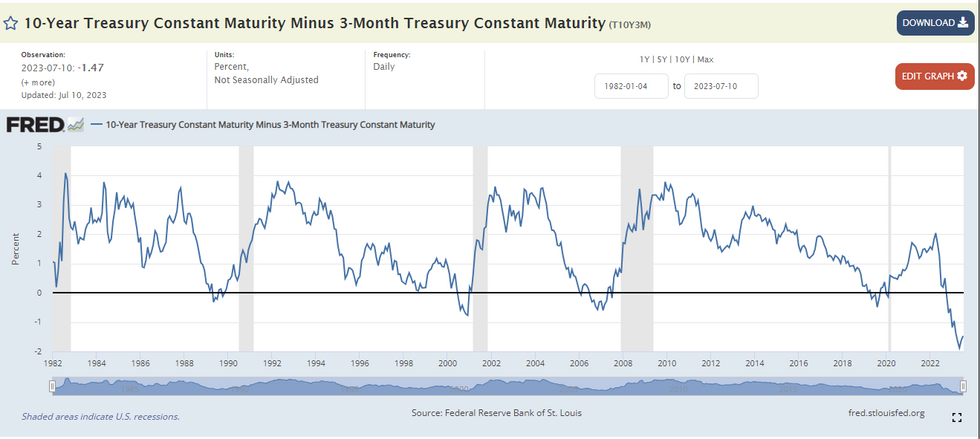

There is such a concern about lending money to invest in the economy that we now have the longest and steepest inversion in the yield curve of U.S. Treasuries. Typically, people are willing to invest money in the short term for lower yields, but expect higher rates of return for longer-term investments. This is why, in a healthy economy, the yield on the 10-year treasury is almost always higher than the yield on the two-year treasury and certainly the three-month bond.

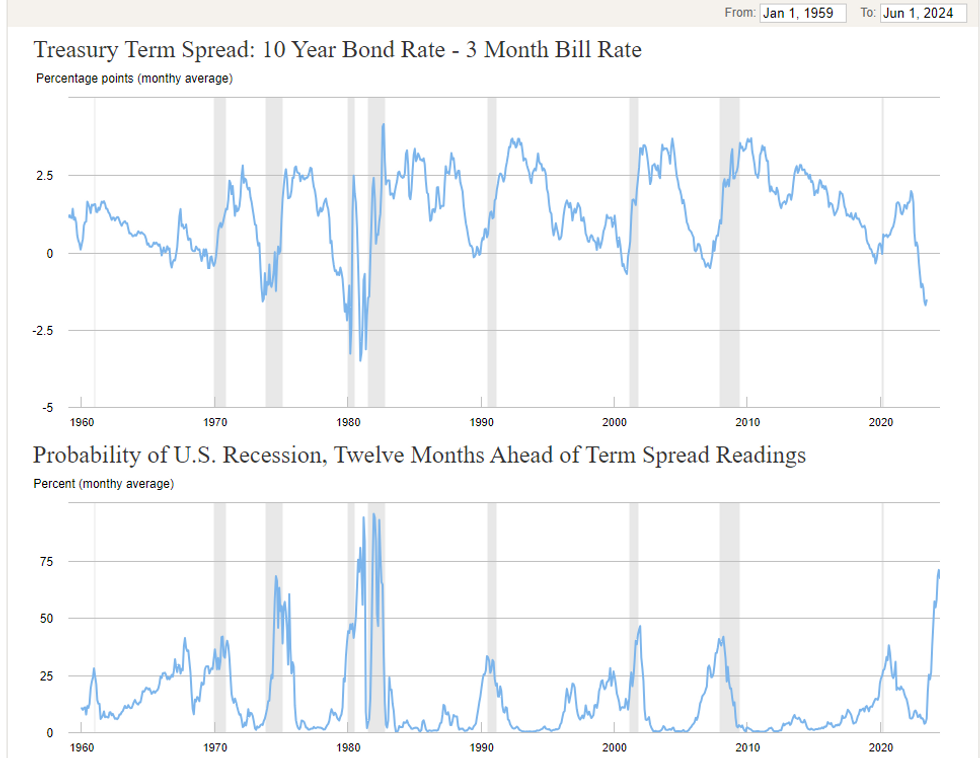

However, during eight periods in history, there has been an inverted yield curve whereby the interest rates are higher on the shorter-term securities. It is known in the financial world as the single best indicator of an impending recession within six to 24 months and has never been wrong. Indeed, it has predicted all eight recessions since the 1960s, including the dot-com bubble bust, the Great Recession, and the COVID recession. The indication of an inverted curve is that investors are flooding longer-term treasuries in anticipation of short-term doom, which creates more demand for 10-year bonds, thereby driving down the yield.

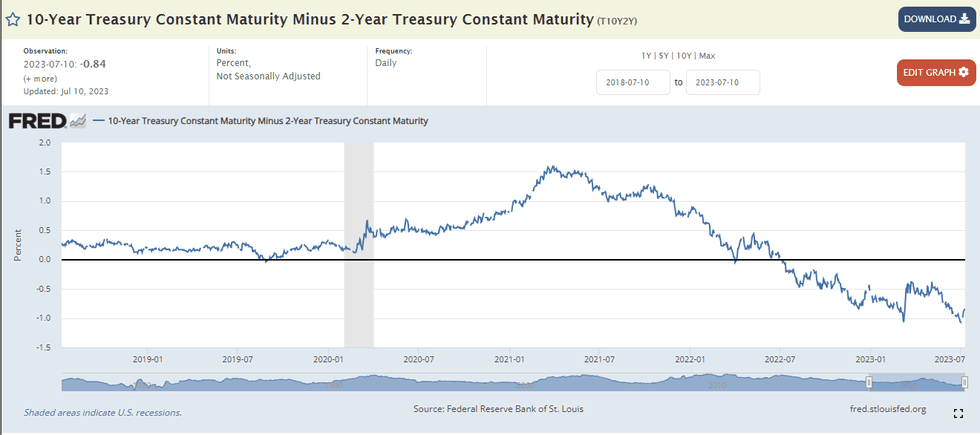

We’ve now been in an inverted curve since last October. As of Tuesday night, the 10-year note stood at 3.96%, the two-year note stood at 4.88%, and the three-month note skyrocketed to 5.45%. That is a 10-year to three-month inversion curve of over 149 basis points. The inversion prior to the 2008 recession was only 60 basis points. The inversion between the 10-month and two-year is the most since 1981.

Here is the 10-year to three-month inversion since October 2022.

And here is the 10-year to two-year inversion, which has now been in place for a full year.

What this means in plain English is that, absent a course correction, the credit market will lock up in the coming months. Investing works on the premise that banks will borrow in the short run to lend in the long run. So typically, you borrow at a lower rate to lend over time at a higher rate. With an inverted yield curve, it is nearly impossible to earn a profit by lending money.

Given that we’ve already been in an inverted curve for nearly nine months, historical trends would point to a recession during the spring of 2024. This is why the New York Federal Reserve now shows a 71% likelihood of recession within the next 12 months based on this leading indicator.

In other words, we are trapped in a vicious cycle of public debt, inflation, higher interest rates, more personal debt, and recession.

There’s also another problem leading to more inflation. The Federal Reserve is being forced to stew in its own trap of the interest rate cliff it created over the past 15 years. The Fed has lost over $50 billion on its balance sheet in the first half of this year, even before we look at its mark-to-market losses approaching $1 trillion as of the end of the first quarter of this year. After all, you can’t hold endless securities at near zero interest and be forced to offload them at 5% and remain solvent. But as American households and small banks go bankrupt from this inversion, the Federal Reserve will just print more money to make up the losses, which will include more – you guessed it – hyperinflation.

All of this cascading effect of carnage is to prop up woke and weaponized government and the debt it accumulates faster than you can say “bankruptcy.”

As CBO warned in its latest long-term budget projection:

“Such high and rising debt would have significant economic and financial consequences. It would, among other things, slow economic growth, drive up interest payments to foreign holders of U.S. debt, elevate the risk of a fiscal crisis, increase the likelihood of other adverse effects that could occur more gradually, and make the nation’s fiscal position more vulnerable to an increase in interest rates.”

That is essentially Bidenomics in a nutshell.