© 2026 Blaze Media LLC. All rights reserved.

There is nothing new about the revised Senate health care bill. It takes all the bad aspects of the original bill and makes them worse, albeit with a phony amendment designed to attract conservatives – an amendment that is nothing more than a talking point.

The core problem with the GOP bill is that it keeps every essential element of Obamacare. The core problem of Obamacare is that after the government already took over half of health care, the ACA made the remainder of the private market so heavily regulated, subsidized, and distorted that nobody could afford either health care itself or medical insurance without government assistance.

Rather than straight up single-payer for the other half of the country (half of health care is already single-payer), Obamacare created a monopoly for a handful of insurers to use the regulations to box out competitors but subsist themselves on guaranteed subsidies and bailouts secured by their lobbyists.

Rather than competing for organic consumer demand, the consumer is completely cut out of the equation; they compete instead for lobbyist-driven subsidies that create a death spiral of monopolies and price inflation.

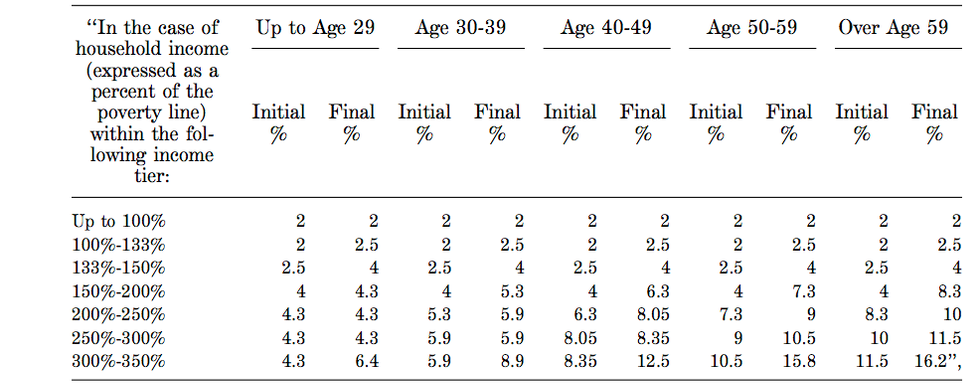

As we demonstrated at the time, the GOP bill keeps all of these elements. Just look at this chart from page six, which shows Stalinist price fixing for how much everyone under a certain income level should pay for government-sponsored and -regulated insurance. The rest of us are left out to dry.

In that respect, Obamacare and Swampcare are even worse than single-payer because those over the subsidy level are not covered and cannot afford health care; they are out of options to purchase affordable insurance as well. This in itself creates a devastating tax cliff, which disincentivizes upward mobility and destroys the economy.

Part of why we never wanted official single-payer is because it’s impossible to then grow the economy beyond 2 percent. Well, the tax cliff from de facto single-payer that leaves out middle class families has created the same economic albatross.

Obamacare and Swampcare are the worst mix of government control and a zombie private market propped up by subsidies but secured as a monopoly through competition-crushing regulations. It has the “greed” of the private sector but lacks the inherent check from the free market of consumer demand because they are sponsored by the endless guarantees from government.

Venture socialism and crony capitalism are worse than straight-up socialism. We get the worst aspects of government control and human nature of the natural market.

Details of the revised Obamacare 4.0 bill

- Keeps tax increases to pay for the entitlement: The revised bill maintains the two largest Obamacare tax increases: the increased Medicare payroll tax and the 3.8 percent surcharge on investment income. That was the only aspect of Obamacare that Republicans universally opposed until now.

- Endless bailouts: In addition, it adds another $70 billion to the existing $112 billion bailout fund for insurers to further inflate the price of insurance and self-perpetuates the need for endless bailouts, which will lead to single-payer.

- More Medicaid spending: The revised bill also throws more money at Medicaid than the previous version (not that any of the baseline rate reductions were going to take place anyway). As I explained before, once you fail to heal the private market, we will all be forced onto Medicaid and there will be no way to reduce the program. Mitch McConnell reportedly admitted that our allegation was correct when he allegedly told a group of liberal Republicans not to worry about the Medicaid cuts because they would never go into effect.

So what is the plan to get conservatives to support what is de facto single-payer? What about the Cruz amendment? Doesn’t it get rid of some of the regulations and will lead to lower premiums?

Not a chance.

In a tried and trusted subterfuge, McConnell took a conservative idea and bastardized it in order to place people like Ted Cruz in a tough position. Yes, technically consumers will be allowed to buy slimmed-down or higher-deductible plans, and (the few remaining) insurers will be allowed to offer them. But they still must offer the regulated plans tailor made through the Obamacare exchanges and subsidized both on the consumer end, on the state end, and on the insurer end.

Thus, the price inflation from the regulations and subsidies will keep premiums high and box out competition from those that lack the economies of scale. Even if they could also provide plans that aren’t “compliant,” they will not be that much cheaper because insurers will have to recoup the losses through healthier people.

In other words, this scheme maintains the original sin of Obamacare: placing everyone in the same pool and forcing the healthy to subsidize the sick, thereby making everyone pay the rate of the sick.

The original plan proposed by conservatives was to have two separate pools whereby sicker consumers would be offloaded into defined contribution subsidies and the rest of the market would be free of regulations AND subsidies in a separate pool. Telling insurers you must keep the insolvent regulations but that they can also have solvent plans is like saying you can carry a bottle of water in one hand if we blow torch your other hand.

Moreover, by keeping the endless subsidies and adding to the bailout fund, this bill ensures that there is no market and organic consumer demand to offer the cheap plans we had before Obamacare.

Everyone else, including healthy families earning under $85,000 or so will still be subsidized and the bailouts will still flow in order to sugarcoat any rate increase, leaving insurers with no deterrent against raising rates. Government will always kick in the rest. The subsidies apply even to those who purchase slimmed-down plans, which will distort their prices.

Here’s an example: At present, I’m paying $1,280 a month for a $13,100 deductible. Before Obamacare, I paid $425 a month for a $5,000 deductible, which, on net, covered more of my basic needs (prior to meeting the deductible) than the Obamacare plan. At the time, we all considered $5,000 to be a high deductible, but it was worth it in exchange for the lower premium.

Obamacare, which is fully kept in place by the GOP bill, has increased deductibles to $13k for a mega premium. Given that the market crisis will not be healed by this amendment, at best they will offer slim plans with a $13,000 deductible for slightly cheaper than the current rate (which is slated to skyrocket further), but well above the pre-Obamacare market.

Is it really worth it for conservatives to have this bill labeled as “the Cruz bill” and incur all the other political liabilities when it won’t fundamentally address the problem with medical insurance or health care?

As I noted before, the compromise solution is to go in the exact opposite direction. Keep the Medicaid expansion (McConnell admitted they are keeping it anyway), fund a separate high risk pool, and leave the rest of us the hell alone. Why are we blowing up the rest of the private market for such a small number of people when 84 percent of those who obtained coverage under Obamacare were thrown onto Medicaid — not private insurance. (Private coverage among those over the age of 26 actually decreased under Obamacare.)

Some might point to the provision Cruz secured in the bill to allow HSAs to cover premium payments as a bright spot. Expanded HSAs is certainly part of the solution after we repeal Obamacare to partially address the overutilization of health insurance and the problems with fourth-party payments so that consumers are directly responsible for their care and will bend the cost of health care itself.

The problem is that until we actually repeal the market distorting and destroying regulations and subsidies, expanded HSAs are tantamount to throwing a diamond on a landfill. We can get a tax exemption to purchase … what?

People are willing to pay more out of pocket to directly pay health care providers assuming they just pay a few hundred a month on catastrophic insurance to cover the a calculated risk. Such an outcome would actually solve the original sin of health care. But this bill will not solve the problem, because even catastrophic insurance will cost too much, rendering HSAs moot.

Passing “something” is not better than nothing. Passing bills is not progress. Doing the right thing is progress.

See More:

20 ideas to crush Obamacare and cure America's health care crisis

The free market solution to pre-existing condition

Government intervention is the cause of health care inflation

A real compromise on health care that would help consumers

Want to leave a tip?

We answer to you. Help keep our content free of advertisers and big tech censorship by leaving a tip today.

Want to join the conversation?

Already a subscriber?