© 2026 Blaze Media LLC. All rights reserved.

One of the major complaints every Republican lodged against Obamacare was that it created the most perverse tax cliff imaginable.

After the actuarially insolvent regulations of Obamacare drove up the cost of insurance, lavish subsidies were given out to those earning below 400 percent of the poverty line to serve as monetary morphine for the self-inflicted cost of the law.

This, in turn, further distorted the market and raised the cost of premiums on those just above the subsidy line, because the subsidies were open-ended rather than a defined contribution.

That is also devastating to the economy, because it discourages productivity and small-businesses growth. While the progressive income tax is anti-growth in itself, there is never a time when you will literally be making less money by earning more income. But with Obamacare, someone who earns a few dollars over the cliff could wind up paying thousands more for insurance.

Let’s explore the math of Obamacare’s tax cliff and compare it to the tax cliff maintained and exacerbated by Trumpcare to demonstrate how Republicans have no intention of repealing the most inimical aspects of the health care leviathan.

A couple will be on their own to pay the Obamacare-driven premiums, whereas families of four earning below $98,000 will already receive some help (while those earning well below that would get significant help).

Picture a husband who earns $60,000 but doesn’t get insurance from work, while his wife is considering starting her own small business at home. Why in the world would she want to earn an extra $40,000 and fall off the cliff?

Now picture a married couple in their 50’s with their kids already moved out of the house. Their subsidies are cut off around $64,000 of income. Not that it’s logical or moral for the government to raise the cost and create a subsidy cliff on anyone, but the Obamacare cliff is a big part of what has turned the backbone of the middle class against Obamacare.

While there are a lot of mini-cliffs throughout the graduated-income scale of subsidies, perhaps the worst is the cliff of 250 percent of the poverty level. Those earning a dollar below that level are eligible for the cost-sharing subsidies that, in addition to reducing premiums, defray the costs of the deductibles and co-payments.

Why would a single 25-year old-male have any incentive to earn more than $30,000 and face the 250 percent cutoff of the cost-sharing subsidy? The point is, unless we are willing to have single-payer, there is no way a fully subsidized and regulated “private” market will ever work.

Now, let’s turn back to Trumpcare. The regulations are not eliminated, and evidently, Republicans are rejecting even Cruz’s mild plan to merely ease some of the regulations while still maintaining the regulated exchanges and subsidies.

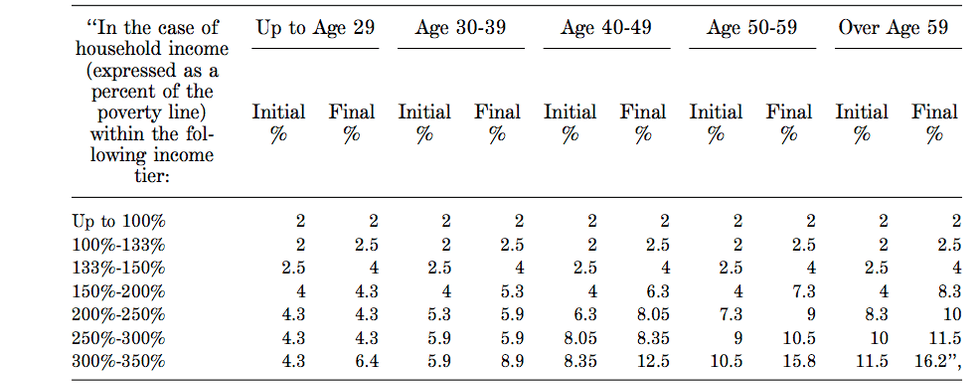

As such, the premiums will not come down. But once again, the subsidies remain, except they draw the line at 350 percent of the poverty line with an even more convoluted tax cliff based on income and age (which reads a lot like Stalin’s five-year price fixing plans).

Thus, most families of four will face the same cliff at roughly $85,000 of household income instead of $98,000 — without actually enjoying lower prices from a healed market, whereby subsidies won’t be necessary. How is this politically defensible? Where is John Kasich’s “moral” outrage over the subsidy tax cliffs created by the government-run health care he so dearly loves?

Take a look at this table taken directly from Section 102 of the Senate health care bill, depicting the price-fixing and social engineering of how much every age and income group is responsible to pay for insurance as a percentage of their income:

This is not the free-market, patient-centered health care Republicans promised; this is as statist as it gets. How about getting rid of the regulations and we won’t need the price-hiking and economically depressing subsidies? What’s so tragic is that we already spend $1.6 trillion on health care, are willing to keep Medicaid expansion, and throw hundreds of billions at new federal high-risk pools to deal with the remaining chronically ill.

Beyond that, is it too much to ask that we have some semblance of a market left without boxing in insurers, but then subsidizing and bailing them out, while locking out middle-income families and taxing economic growth?

Every Republican understood this argument as it related to Obamacare, but somehow they are embracing the tax cliff with Trumpcare.

This is why it’s so absurd for Republicans to advertise they are eliminating the Obamacare tax increases while they are keeping the core of Obamacare itself. The regulations and the subsidies of Trumpcare are much more expensive than the Obamacare tax hikes. And, unlike the official Obamacare tax hikes, they crush middle-income families earning between $100,000 and $200,000 a year.

Undoubtedly, this is a big reason why the economy is stuck at 1 percent growth and why it will remain that way until Obamacare is repealed. It’s absurd to promise “tax reform” as an engine for economic growth while they are embracing, codifying, and exacerbating Obamacare’s regulatory/subsidy tax cliff (which is a more potent variable weighing down the economy than marginal income tax rates).

We already have 55 percent of health care that is government-run. There is no way to keep the remaining portion solvent without a free market. It’s either single-payer or free market. A zombie private sector devastated by regulations and market distortions but propped up by government subsidies and bailouts is unsustainable.

That is why both Obamacare and Trumpcare should be a non-starter.

Want to leave a tip?

We answer to you. Help keep our content free of advertisers and big tech censorship by leaving a tip today.

Want to join the conversation?

Already a subscriber?